Life insurance is one of the most important financial tools for seniors to ensure that their loved ones are financially protected in the event of their passing. As you age, finding the right life insurance plan becomes increasingly important, whether you are looking to cover final expenses, provide financial security for your family, or leave a legacy. MyWebInsurance.com Life Insurance Plans For Seniors is an excellent platform that helps seniors navigate through these options, compare quotes, and find the best policy to meet their unique needs.

Stay tuned with us as we will guide you through everything you need to know about life insurance for seniors, including the different types of plans available, key factors to consider, and how MyWebInsurance.com can help simplify your decision-making process.

How Does Life Insurance Work For Seniors, And What Should They Know?

Life insurance for seniors differs from traditional policies aimed at younger individuals. As health risks and financial priorities evolve, seniors need plans tailored to their stage in life. Whether it’s to cover funeral costs, pay off remaining debts, or leave an inheritance, the right policy ensures your loved ones are financially protected.

Platforms like mywebinsurance.com serve as valuable resources, helping seniors compare options from multiple insurance providers efficiently. While mywebinsurance.com itself may not sell policies directly, it provides tools, resources, and partnerships with insurers to help seniors find coverage suited to their needs.

What is MyWebInsurance.com?

“MyWebInsurance.com serves as a digital insurance marketplace, not as a direct insurance provider. This means that it offers a platform where seniors can compare life insurance quotes and policies from various reputable insurance providers. It’s an excellent resource for exploring your options without having to directly contact multiple companies.

The platform allows you to evaluate various types of policies, premiums, and benefits from a variety of carriers, ensuring you get the best deal tailored to your needs. With just a few clicks, you can quickly find and compare plans, saving time and effort while making an informed decision. It’s all about making the process simpler and more accessible for you.”

Why Seniors Should Consider Life Insurance?

Life insurance for seniors goes beyond simply paying for funeral costs—it provides financial security, peace of mind, and strategic benefits.

- Cover End-of-Life Expenses: Funeral costs in the U.S. average between $8,000 and $12,000. Final expense insurance ensures your loved ones aren’t left with this burden.

- Debt Protection: Outstanding mortgages, credit cards, and medical bills can be paid off using life insurance proceeds. This prevents families from facing financial strain during a difficult time.

- Legacy Planning: Seniors can designate beneficiaries, including children, grandchildren, or charities, ensuring that their assets support loved ones even after their passing.

- Peace of Mind: Knowing your financial responsibilities are covered reduces stress for both you and your family. Seniors can enjoy retirement without worrying about what will happen after they’re gone.

- Financial Flexibility: Many policies allow access to cash value, policy loans, or partial withdrawals to address unexpected expenses, making them versatile tools for seniors.

Practical Tip: Seniors should start by assessing their top financial priorities—whether it’s covering end-of-life expenses, leaving a legacy, or ensuring debt-free closure for their family. This helps in selecting the most appropriate plan.

Life Insurance Options For Seniors – What’s Available?

When it comes to MyWebInsurance.com Life Insurance Plans For Seniors, there are a few main types of policies that seniors typically consider. Each plan has its own advantages, depending on your needs, health, and budget. Let’s explore the most popular options:

Whole Life Insurance:

Whole life insurance is designed for seniors who want lifetime coverage and guaranteed payout for their beneficiaries. It provides coverage for as long as you live, and the premiums generally stay the same throughout your life. Plus, a whole life policy builds cash value over time, which you can borrow against if needed.

- Pros:

- Lifetime coverage and guaranteed payout

- Builds cash value over time

- Fixed premiums that don’t increase as you age

- Cons:

- Higher premiums compared to other options

- May not be affordable for those on a fixed income

This is ideal if you’re looking for long-term financial security for your loved ones.

Final Expense Insurance:

Final expense insurance is a type of whole life insurance designed specifically to cover funeral costs and other end-of-life expenses. This plan is perfect for seniors who want to make sure their family isn’t burdened with funeral expenses.

- Pros:

- Lower premiums compared to whole life insurance

- No medical exam required in most cases

- Helps cover funeral and burial costs

- Cons:

- Lower coverage amounts (typically between $5,000 and $25,000)

- Limited to funeral expenses

If you’re mainly concerned about ensuring your funeral expenses are covered, this option might be the best for you.

Term Life Insurance:

Term life insurance is designed to cover a specific period, such as 10, 20, or 30 years. If you’re looking for temporary coverage or want an affordable option to cover a mortgage or other obligations, term life insurance is a great choice.

- Pros:

- Lower premiums than whole life insurance

- Provides coverage for a specific period (ideal for short-term needs)

- Cons:

- No cash value or permanent coverage

- Can get expensive if you renew the policy after it expires

Term life is perfect if you only need coverage for a set time, like covering your mortgage or ensuring your spouse has financial support after your passing.

Guaranteed Acceptance Life Insurance:

Guaranteed acceptance life insurance guarantees coverage regardless of your health status. This is a good option for seniors with pre-existing health conditions who might struggle to get approved for traditional life insurance.

- Pros:

- No medical exam or health questions

- Guaranteed acceptance, even for those with health issues

- Fast and easy approval process

- Cons:

- Higher premiums compared to other options

- Lower coverage amounts (often only $5,000 to $25,000)

- Coverage starts after 2-3 years (depending on the insurer)

If you have health concerns or find it difficult to qualify for traditional life insurance, this type of policy is an excellent way to ensure you have coverage.

How Do Seniors Choose the Right Life Insurance Provider?

Finding the right provider matters as much as choosing the policy. For seniors, it’s about reliable coverage, easy applications, and peace of mind. Mywebinsurance.com connects you to trusted insurers to compare and find the best fit.

Fidelity Life:

Fidelity Life is a strong choice for seniors looking for coverage up to age 85. The application process is straightforward, and the company offers plans tailored to address health concerns, making it easier for older adults to secure coverage without hassle.

MassMutual:

MassMutual is well-known for its whole life insurance plans. Their Whole Life 100 policy ensures lifelong coverage, allowing seniors to protect loved ones well into their later years. With stable premiums and the option for cash value growth, it’s ideal for seniors who want long-term security and financial planning benefits.

Mutual of Omaha:

Mutual of Omaha stands out for its high age limits and flexible premium options. Seniors can customise policies to meet their needs, whether they want temporary protection or permanent coverage. The company is recognised for its strong reputation and responsive customer service, giving peace of mind to policyholders.

Gerber Life:

Gerber Life offers simplicity and affordability. Most of their senior plans require minimal medical information, making it accessible for those with health conditions. With straightforward policies and reasonable premiums, Gerber Life is a practical choice for seniors seeking essential coverage without complications.

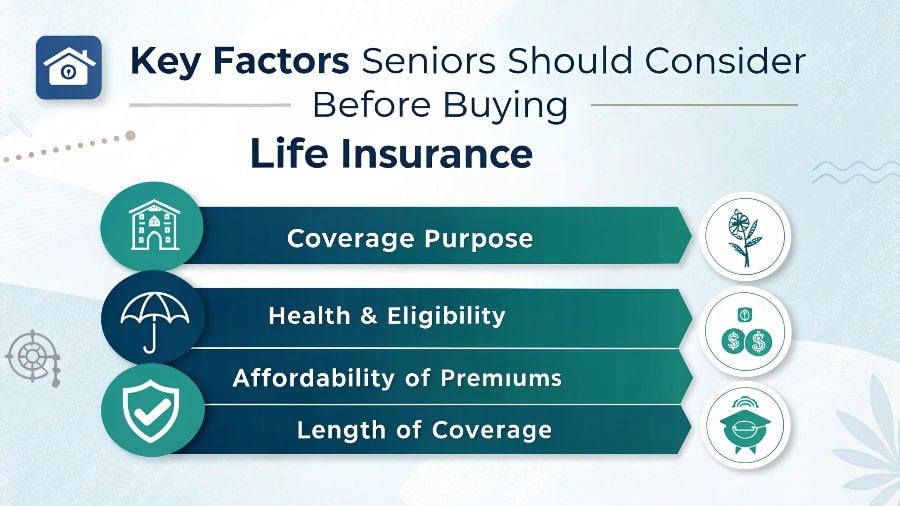

What Key Factors Should Seniors Consider Before Buying Life Insurance?

When exploring mywebinsurance.com life insurance plans for seniors, it’s important to weigh more than just the price. Seniors should carefully consider the following points before finalizing a policy:

- Coverage Purpose: Decide whether you want the policy to cover end-of-life expenses, provide income replacement, or leave a legacy for loved ones. Clear goals help in selecting the right type of insurance.

- Health & Eligibility: Some policies require medical exams, while others offer simplified or guaranteed issue options. Your health condition will directly impact your eligibility and premium costs.

- Affordability of Premiums: Look at what you can comfortably pay each month or year without financial strain. Affordable premiums ensure you can keep your policy active long term.

- Length of Coverage: Choose between temporary protection (term life) or lifelong security (whole or guaranteed universal life). Seniors often prefer permanent coverage to avoid outliving a policy.

- Provider Reliability: Pick insurers with strong reputations, financial stability, and good customer support. Reliable providers give seniors confidence that claims will be honoured promptly.

- Policy Features & Flexibility: Some plans include cash value growth, accelerated death benefits, or flexible premiums. These features can add extra security and value to your coverage.

The Latest Trends and Options in Senior Life Insurance – Don’t Miss Out!

Life insurance for seniors is evolving. Here are some insights and perspectives not widely discussed:

| Angle / Trend | Description | Benefits for Seniors |

|---|---|---|

| Digital Platforms | Websites like mywebinsurance.com allow seniors to compare policies from multiple providers online. | Saves time, reduces paperwork, and helps find the best fit based on age, health, and budget. |

| Health & Wellness Incentives | Some insurers offer discounts or rewards for healthy lifestyles, non-smoking, or regular checkups. | Encourages healthy habits and can reduce premiums or provide extra benefits. |

| Hybrid Policies | Combines life insurance with long-term care coverage. | Provides financial protection for medical expenses while maintaining a death benefit. |

| Legacy & Estate Planning | Policies can fund charitable contributions, trusts, or educational funds for grandchildren. | Allows seniors to leave a meaningful legacy and support loved ones financially. |

| Simplified Applications / Guaranteed Acceptance | No-medical-exam or guaranteed issue policies for seniors. | Quick approval and accessible coverage even with health concerns or age restrictions. |

How to Get Started with MyWebInsurance.com Life Insurance Plans for Seniors?

Getting started with MyWebInsurance.com is simple. Follow these steps to begin comparing life insurance quotes for seniors:

- Visit MyWebInsurance.com: Go to the website and select the “Life Insurance for Seniors” section.

- Enter Your Information: Fill in the required details, such as age, health status, and the coverage amount you’re seeking.

- Compare Quotes: The platform will generate a list of insurance options from various carriers, allowing you to compare premiums, coverage, and other factors.

- Choose the Best Plan: After reviewing the quotes, select the plan that best suits your needs and budget.

- Apply for Coverage: Once you’ve chosen a policy, you can apply directly through the platform or be connected with a licensed insurance agent for further assistance.

Benefits Of Choosing MyWebInsurance.com – Why Seniors Love It For Life Insurance!

Choosing mywebinsurance.com makes finding life insurance for seniors simple and stress-free. The platform allows you to compare multiple providers and policies in one place, saving time and effort. You can filter options by age, coverage amount, and premium, making it easier to find a plan that fits your needs and budget. Seniors also benefit from clear, easy-to-understand information about different types of policies, helping them make informed decisions.

The site connects you to trusted insurers, ensuring reliability and peace of mind. Plus, the online application process is straightforward, reducing paperwork and hassle. Overall, mywebinsurance.com provides a convenient, transparent, and efficient way for seniors to secure the right life insurance coverage.

What Are The Common Misconceptions About Senior Life Insurance?

Many seniors hesitate to buy life insurance due to common myths and misunderstandings. Here are some of the most common misconceptions:

- Life Insurance Is Too Expensive: Many assume premiums are unaffordable, but options like final expense or simplified issue plans offer reasonable rates for seniors.

- Health Issues Prevent Coverage: Even seniors with chronic conditions can often qualify for no-medical-exam or guaranteed acceptance policies.

- Term Insurance Isn’t Useful for Seniors: Although term insurance is temporary, it can still cover specific financial responsibilities, such as mortgages or debts.

- Life Insurance Is Only for Young Families: Seniors use policies to cover end-of-life expenses, provide for a spouse, or leave a legacy—not just to support children.

- It’s Too Late to Get Coverage: Seniors can still obtain policies even in their 70s or 80s, especially through providers offering high age limits or simplified applications.

- All Policies Are the Same: Coverage, premiums, and benefits vary widely between providers and policy types, so comparison is crucial to find the right fit.

Tip: Understanding these misconceptions helps seniors make informed decisions without unnecessary worry or hesitation.

Tips For Seniors Applying For Life Insurance – Maximize Your Approval Chances!

When applying for life insurance as a senior, it’s important to take a few steps to increase your chances of approval. First, be honest about your health and medical history, as insurers will assess these factors to determine your premiums. Consider choosing guaranteed acceptance life insurance if you have health concerns, as this type of policy doesn’t require a medical exam.

Also, shop around and compare quotes from multiple providers to find the best rates. It’s helpful to start early, as premiums may increase with age. Lastly, review policy options carefully to choose the one that fits your financial and coverage needs. Taking these simple steps can help ensure you get the right coverage at a price you can afford.

How To Compare Senior Life Insurance Plans?

Choosing the right plan can be overwhelming, but seniors can make an informed decision by focusing on a few key factors. Here’s a practical step-by-step guide:

- Use Online Comparison Tools: Websites like mywebinsurance.com aggregate multiple insurers and plan options in one place. This saves time and helps seniors quickly identify policies that fit their age, health, and coverage needs.

- Evaluate Premiums vs. Coverage: Compare the cost of premiums against the benefits offered. A higher premium may provide lifelong coverage or cash value accumulation, while lower premiums may suit temporary needs.

- Check Age Limits and Eligibility: Some policies have maximum issue ages. Make sure your chosen plan allows enrollment at your current age and consider simplified issue or guaranteed acceptance options if you have health concerns.

- Assess Policy Features: Look for features like cash value accumulation, flexible premiums, or accelerated death benefits. These can add extra value and security to your coverage.

- Review Exclusions and Waiting Periods: Understand any limitations, such as pre-existing condition clauses, waiting periods before full benefits are paid, or policy exclusions. This prevents surprises later on.

- Compare Provider Reputation: Research insurer ratings, financial stability, and customer service quality. A reputable provider ensures claims are handled efficiently and reliably.

- Consider Your Long-Term Goals: Think about whether you want coverage for a short-term financial need or lifelong protection. Align the policy with your retirement plans, legacy goals, and family responsibilities.

- Seek Expert Advice if Needed: Consult a licensed insurance agent or financial advisor for guidance. They can help interpret policy details and recommend options suited to your unique situation.

FAQs:

How much coverage do seniors usually need?

Coverage depends on goals, such as covering funeral costs, paying off debts, or leaving a legacy. Many seniors opt for $10,000–$50,000 for final expenses or higher for permanent plans. Analyzing personal financial obligations helps determine the right amount.

Does mywebinsurance.com sell life insurance directly to seniors?

No, mywebinsurance.com does not sell policies directly. Instead, it acts as a comparison platform, helping seniors explore options from multiple insurance providers. This approach allows seniors to make informed choices without visiting multiple insurance offices.

Can seniors get life insurance without a medical exam?

Yes, certain policies like final expense or simplified issue life insurance typically do not require a medical exam. Eligibility is often determined through a health questionnaire. This makes it easier for seniors with pre-existing conditions to secure coverage quickly.

Is cash value accumulation available in senior life insurance?

Yes, whole life and guaranteed universal life policies accumulate cash value over time. This cash value can be borrowed against or withdrawn for emergencies. It provides a financial cushion beyond the death benefit.

Can I combine multiple policies for better coverage?

Combining policies, such as a small final expense plan with a whole life or term policy, is possible. This approach balances affordability and comprehensive coverage. Seniors can tailor coverage to specific financial needs.

Conclusion:

For seniors, securing life insurance is more than a financial transaction—it’s a step toward peace of mind, legacy planning, and ensuring loved ones are protected. By leveraging mywebinsurance.com’s life insurance plans for seniors, individuals can access multiple providers, compare policies, and make informed decisions tailored to their unique needs. Whether you are considering final expense insurance, whole life, or guaranteed universal life, understanding the nuances of each policy, evaluating provider reputations, and considering your financial goals ensures you select the coverage that truly fits your life stage.

With careful planning and informed decision-making, seniors can confidently safeguard their future and provide financial security for those they care about most.

Also Read: